Covariance is a measure of the strength of a linear relationship between two continuous random variables (essentially how much they vary together). For example, if one variable increases as the other decreases, then the two variables covary. If one variable doesn’t change while the other increases, then they do not covary.

The numerator is the sum of coross-products (the bivariate analogue of the sum of squares (ss). Covariance ranges from to .

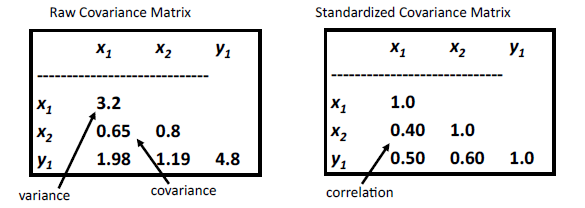

One limitation is that the absolute magnitude of the strength of a linear relationship depends on the units in the two variables. If you standardise the covariance by dividing by the standard deviations of the two variables so that the measure lies between -1 and +1 then you get the Pearson correlation. The Pearson correlation measures the “strength” of the linear relationship between Y1 and Y2.

One limitation is that the absolute magnitude of the strength of a linear relationship depends on the units in the two variables. If you standardise the covariance by dividing by the standard deviations of the two variables so that the measure lies between -1 and +1 then you get the Pearson correlation. The Pearson correlation measures the “strength” of the linear relationship between Y1 and Y2.

The sample correlation coefficient (r) is also the sample covariance of two variables that are both standardized to zero mean and unit variance. The population correlation coefficient () is not quite the same thing as r. If our sample data comprise a random sample from a population of pairs ( then the sample correlation coefficient is the maximum likelihood estimator of the population correlation coefficient (r will slightly under-estimate p, although the bias is small).

Covariances are often used to fit models, but the standardised covariances (or correlations) are used for interpretation. This is because correlations have less information (they tell you the direction and the spread of the data) but they are directly comparable. Covarainces cannot be compared unless they have the same units.

Covariances are often used to fit models, but the standardised covariances (or correlations) are used for interpretation. This is because correlations have less information (they tell you the direction and the spread of the data) but they are directly comparable. Covarainces cannot be compared unless they have the same units.

This was taken from a lecture from An Introduction to Structural Equation Modeling for Ecology & Evolutionary Biology. http://byrneslab.net/teaching/sem/

This information was taken from the book: Quinn and Keough (2002) Experimental design and data analysis for biologists. Cambridge University Press.

RSS Feed

RSS Feed